6 Settlements patterns for 2021

In 2015 was a transformational year for the settlements landscape. Settlement networks progressed to satisfy client need, and also developing dangers of the COVID-19 infection.

Clients throughout the age range promptly adjusted to electronic, contactless repayment networks as social distancing regulations were enforced for public security.

According to a JP Morgan research study launched in Dec. 2020, “54 percent of customers concurred that they utilize electronic financial devices a lot more as a result of the pandemic today than they did in 2015.”

A requirement and also assumption for real-time settlements additionally emerged as financially-strained individuals looked for accessibility to their funds with even more necessity.

” The pandemic increased a great deal of patterns that were capturing grip the year prior,” Forrester expert Lily Varon informed sis magazine Settlements Dive. “Advancement from both the vendor and also client side grabbed speed to advance with altering market problems.”

Below are the leading 6 repayment patterns that got grip in 2020 and also are readied to advance right into conventional repayment versions this year.

1. Credits or purchase currently, pay later on

Electronically delayed settlements have actually been obtaining appeal amongst individuals considering that 2019. In 2020, when funds were particularly limited, consumers rotated to the buy currently, pay later on (BNPL) repayment techniques.

” As individuals coped the pandemic, purchase currently, pay later on came to be a substantial fad, installing that within the getting that check out,” Brandon Rembe, primary item police officer at Envestnet-Yodlee, informed Settlements Dive. “BNPL is enabling business to service those kinds of customers that do wish to pay gradually.”

There has actually been a substantial modification in the classification as well as additionally simply a basic need to eliminate rubbing around settlements. Clients desire a smooth repayment network, while services wish to hang on to their client base and also lower deal prices, Rembe claimed.

According to a Forrester webinar, almost “36% people on the internet grownups want, presently utilize, or have actually utilized a “purchase currently, pay later on” solution for a big acquisition.”

Vendor fostering for such solutions has actually additionally boosted as they are attempting to satisfy client needs for BNPL repayment offering.

” In Jan 2020, 26% of the 100 united state sellers provided a credit approach,” the Forrester webinar specified. “By December, that number had actually boosted to 46%.”

” The pandemic increased a great deal of patterns that were capturing grip the year prior … Advancement from both the vendor and also client side grabbed speed to advance with altering market problems.”

Lily Varon

Expert, Forrester

Standard sellers Macy’s, Space and also Neiman Marcus have actually begun providing BNPL to bank card averse consumers. ” Lots of consumers are making use of these solutions for much better budgeting factors,” Varon claimed. “You can purchase even more and also spread it throughout a longer amount of time.”

BNPL business consisting of Klarna, Affirm, Uplift and also Splitit experienced substantial development in 2020 as consumers’ buying power dipped as a result of the pandemic. Splitit saw its client base double while experiencing a 300% boost in income throughout 2020. Splitit additionally presented BNPL solutions to the expert solutions market in 2015, including the alternative for consumers to spend for expert solutions– such as accountancy, oral and also lawful solutions– in installations.

BNPL solutions have actually been obtaining energy considering that prior to the pandemic, yet the boosted use ecommerce in 2015 fast-tracked client fostering in the direction of installation settlements, Brad Paterson, Chief Executive Officer of Splitit, informed Settlements Dive.

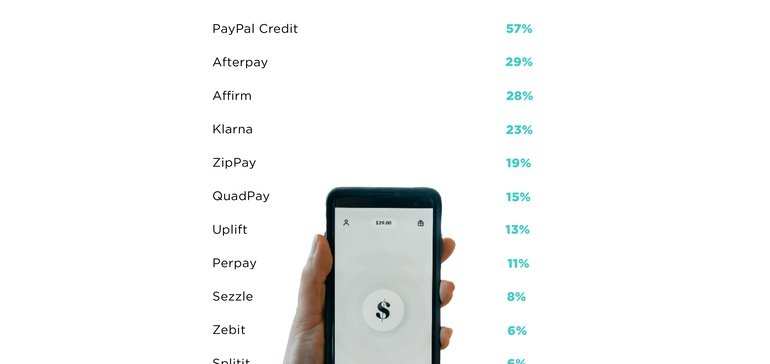

Affirm went public at the beginning of this year to lean right into its development, and also also launched an Affirm card for consumers to have even more choices for BNPL solutions. Virtually 13% of united state BNPL consumers had actually utilized Affirm in Q42020, contrasted to 7% in Q12020.

Equity capital financing for BNPL solutions additionally increased in the previous 2 years as this repayment network got consumers. According to Forrester research study, VC financing for BNPL solutions leapt to $1.9 billion in 2020 from $1.8 billion in 2019, and also up from $302 million in 2018.

While more youthful generations that are bank card averse moved to BNPL solutions, the fostering of this repayment network allures throughout the age range.

” Our information kind of programs that rate of interest definitely is focused on the more youthful teams,” Varon claimed. “Yet really, uses correspond throughout age.”

Recognized repayment titans Visa, Mastercard and also PayPal (Pay in 4) have actually additionally begun providing BNPL solutions to satisfy developing customer need.

While BNPL solutions are obtaining appeal and also grip amongst customers and also services alike, they include strings connected. Many individuals do not totally recognize the BNPL solution offering and also obtain stalled with surprise charges when they miss out on a repayment. Returning an item acquired via such repayment choices is additionally commonly harder for a customer.

According to a current study in the UK, almost 20% of consumers that went with BNPL solutions for Xmas purchasing are having a hard time to pay on schedule. Such offerings can lead individuals to outspend their spending plans and also harm their debt rankings when they miss out on settlements.

In the united state, BNPL has actually been flying under the radar as it’s still in its very early fostering phases. BNPL might be based on analysis from the Federal Profession Compensation (FTC) and also Customer Financial Defense Bureau (CFPB), which supervise borrowing techniques for Unfair, Deceitful or Violent Acts or Practices (” UDAAP”), if customers are negatively influenced by the repayment offerings.

2. Digital settlements

According to virology researches, the COVID-19 infection can endure on banknotes for approximately 28 days, engaging customers to pivot to electronic repayment networks to stay clear of having and also spreading out the infection.

Customers adjusted making use of electronic repayment networks such as tap-to-pay, ecommerce and also electronic purse settlements to stay clear of call while making a repayment. Mobile settlements and also electronic budgets were 2 of one of the most prominent repayment kinds as they overshadowed cash money purchases in 2020, according to a FIS record.

” Mobile purse deal counts increased in the months adhering to March 2020,” David Carrier, an Aite expert, informed Settlements Dive.

A Fiserv research study specified almost 24% of participants thought mobile settlements were the best to stop the spread of the infection.

” Card providers wish to be ‘top of the mobile purse,'” Carrier claimed. “They are motivating cardholders to include their card to their mobile purse.”

There are numerous advantages for card providers to provide electronic cards and also electronic budgets. Greater protection brings about greater use, enhancing the probability the cardholder will certainly bring a charge card equilibrium, according to Aite research study.

” Card providers wish to be ‘top of the mobile purse.'”

David Carrier

Expert, Aite

Digital purse individuals are anticipated to surpass 4.4 billion internationally by 2025, up from 2.6 billion in 2020, Juniper research study specified. The complete quantity invested via electronic budgets is additionally anticipated to almost increase to $10 trillion every year by 2025 from $5.5 trillion over the moment duration.

In the united state, almost $131.4 billion was invested via mobile settlements, with 86.9 million individuals in 2020, up concerning 20% in buck worth from $110.5 billion, with 71.5 million individuals in 2019, according to eMarketer approximates from Expert Knowledge.

” Mobile purse energetic cards are still much less than 10% of complete cards, so there is a great deal of area to expand,” Carrier claimed. “There will certainly be proceeded development in mobile purse settlements and also electronic card issuance.”

Although increasing, mobile purchases are vulnerable to be targets of cyberattacks. Digital purse purchases saw a 33% boost YoY in fraudulence efforts, while the ordinary quantity swiped from such purchases up by 9% YoY too, according to a current record from the electronic fraudulence avoidance business Look. Customer issues to the CFPB additionally climbed by 59% YoY relating to mobile and also electronic money purchases.

Firms such as PayPal brought out QR codes to offer various other electronic repayment networks for consumers and also vendors alike. PayPal and also Venmo’s QR codes are approved at over 600,000 retail places, Jim Magats, elderly vice head of state of omni settlements at PayPal, informed Settlements Dive.

” PayPal authorized 29 huge ventures like CVS, Nike, Macy’s and also Foot Storage locker to its QR repayment network in 2020,” Magats claimed. “We are seeing a 19% boost [year-over-year] in complete settlements quantity for customers that utilize our OR codes.”

According to a McAfee record, climbing mobile and also QR code-based settlements are not as risk-free as they may appear. QR codes offer fraudsters with a brand-new method for camouflaging themselves as genuine services and also spreading out destructive web links.

Sound-based repayment networks are getting grip as they can refine settlements from further away, with very little brand-new software and hardware remedies. LISNR, a Visa-backed technology start-up that utilizes ultrasound innovation for mobile verification and also settlements, experienced a close to 300% boost in deal quantity quarter over quarter throughout the pandemic.

3. Surge of ecommerce and also ingrained settlements

united state retail ecommerce sales grabbed throughout the lockdown as even more individuals went shopping online. In 2020, $794.5 billion was invested via ecommerce networks, rising 32.4% every year over 2019. Shopping sales comprised 14.4% of all sales in the united state in 2015, contrasted to 11% in 2019.

Amidst shop closures, sellers increase their ecommerce visibility, consisting of small companies that had not offered online prior to. According to electronic settlements business Square, the share of services approving on the internet settlements boosted by 13.2% from February to July 2020.

Also in fields that had not made much use the network, such as in sales of grocery stores and also drinks, acquisitions expanded 74% YoY in 2020, a price greater than three-way that of 2019, Expert Knowledge record specified.

Shopping fostering climbed up throughout the age range. Before the pandemic, older consumers formerly went shopping online at a lot reduced prices than more youthful grownups. Yet senior citizens, that are most in jeopardy from the infection, looked to electronic methods to lower the health and wellness threat.

” We have actually type of constantly really felt that customers were quite sluggish at embracing brand-new financial and also repayment routines,” Sarah Grotta, Supervisor of Debit and also Choice Products Advisory Solution at Mercator Advisory Team, claimed throughout a webinar. “Yet, we actually saw that customers, consumers and also participants will really alter their routines quite promptly, out of need, or often, when the appropriate motivation is placed in front of them.”

Simply 16% of net individuals over 65 went shopping online at the very least as soon as a week in May 2019, “yet 43% of that market reported doing so a lot more often than in the past in 2020,” Expert Knowledge record specified.

” united state retail ecommerce sales will certainly make up $1 in $5 invested in retail by 2024.”

Expert Knowledge

While in-store retail is bound to grab as the pandemic subsides, the occasions of 2020 increased the change to ecommerce by concerning 2 years, according to an Expert Knowledge record.

” united state retail ecommerce sales will certainly make up $1 in $5 invested in retail by 2024,” the record specified. “They’ll make up $1.205 trillion, as on the internet purchasing experiences enhance, stores close at document prices, and also consumers preserve routines built in 2020 and also 2021.”

4. Real-time settlements and also ACH purchases

When funds were particularly limited around the world, customers desired accessibility to their funds immediately. With the increase of peer-to-peer settlements (P2P), services additionally began anticipating transfer to be a lot more reliable and also as fast as PayPal or CashApp transfers.

According to a JP Morgan research study, job economic situation employees, insurance coverage plaintiffs and also tiny and also mid-sized services (SMBs) anticipate to get and also access their funds instantly.

Greater than 70.3 billion real-time repayment purchases were refined internationally in 2020, a rise of 41% contrasted to the previous year, according to an ACI Worldwide research study. With almost 2 billion real-time repayment purchases refined in 2020, The United States and Canada is forecasted to be the highest possible development area by 2025, the research study specified.

” In the united state, we actually didn’t have a demand for real-time settlements for a very long time … Yet that is beginning to alter, as individuals are anticipating even more and also banks see a benefit to pay quicker.”

Sarah Grotta

Supervisor of Debit and also Choice Products Advisory Solution, Mercator Advisory Team

Clients are rotating to P2P applications for immediate purchases as numerous banks do not have the facilities to sustain real-time settlements. According to a Mercatory study, 70% of financial institution consumers have actually utilized a P2P solution at the very least as soon as in the previous year, Grotta claimed.

” You have a look at the variety of cash activity purchases that you as a banks may not be taking part in since your participants need to go elsewhere,” Grotta claimed. “It actually does make you [financial institutions] think of this, this might be a rather vital option to provide.”

Virtually 60% of the united state market anticipates real-time settlements, according to the JP Morgan research study. Lots of nations like the UK have actually been providing real-time settlements considering that 2008, yet “in the united state is the level of intricacy arising from a much majority of financial institutions than in various other nations,” the research study specified.

” In the united state, we actually didn’t have a demand for real-time settlements for a very long time,” Grotta claimed. “Yet that is beginning to alter, as individuals are anticipating even more and also banks see a benefit to pay quicker.”

The existing clearinghouses are had by the biggest banks in the nation like Wells Fargo, Financial Institution of America and also CitiBank, inhibiting smaller sized banks from signing up with the network since they do not wish to utilize a rival’s solutions and also spend for it, Grotta claimed.

The Reserve Bank has actually begun the FedNow task, which will certainly bring all banks right into a real-time repayment network. Virtually 200 banks, consisting of Visa, Mastercard and also Temenos, have actually signed up with the task to aid the Fed produce a system that collaborates with all banks throughout the nation, 365 days a year to offer real-time settlements.

Automated removing home (ACH) network settlements additionally saw an uptick in 2020, as debt and also debit purchases grabbed as a result of on the internet purchasing. Lots of business-to-business (B2B) settlements additionally rotated to ACH settlements, as it normally sets you back much less than $1 per deal, “making it an attractive alternative, specifically for high-value transfers,” Expert Knowledge record specified.

ACH was produced to electronically change financial institution checks, yet has actually swelled in purchases as a result of fast handling time and also inexpensive connected with it. In spite of sluggish financial task, ACH settlements wrecked documents in 2020, enhancing by 8.2% to 28.6 billion purchases, according to Nacha.

5. Advancement of P2P settlements

P2P settlements began obtaining appeal after the 2008 monetary dilemma, getting substantial energy throughout the 2020 pandemic too. What began as a reliable, simple and also fast approach to move funds and also split pizza expenses amongst peers has actually changed right into a multi-facet system, offering virtually as a financial institution.

Venmo, Zelle, and also Square Cash money applications have actually expanded in appeal, with quantity striking $393.9 billion on the back of large customer development in 2020, Expert Knowledge record specified.

” We saw a 24% boost of energetic accounts, virtually 73 million internet brand-new accounts included, and also almost 41 repayment purchases per account, all leading up to $936 billion in complete repayment quantity in 2020,” PayPal’s Magats claimed.

Before the pandemic, mobile P2P development had actually been slowing down as usage amongst more youthful consumers– its leading market– came to be prevalent. Yet with the pandemic, quantity got to $393.9 billion in 2020, up 5% from $375.1 in 2019, and also is anticipated to strike $538.7 by the end of 2022. The variety of individuals additionally boosted from 79 million in 2019 to 82 million in 2020 and also is anticipated to strike 100 million by the end of 2024.

Gains were moved by older consumers particularly, that crowded to the solutions to change cash money and also checks. Lots of repayment systems given added solutions like financial investment and also trading, cryptocurrency purchases and also debit card offerings to maintain consumers.

” The majority of electronic P2P applications are seeking means to create income and also are providing bank-like services and products to drive income,” Talie Baker, an elderly expert at Aite claimed. “PayPal, Venmo, and also CashApp have actually all ventured right into crypto trading as a method to create income.”

PayPal thinks electronic money, reserve bank electronic money and also the cooperation with reserve banks and also regulatory authorities will certainly open up brand-new means to exchange worth and also power worldwide business and also monetary solutions. It has actually additionally assisted in including and also keeping consumers on the system.

” Clients that have actually bought crypto have actually been logging right into PayPal at about two times their login regularity before buying crypto,” Magats included.

P2P additionally assisted offer SMBs throughout the pandemic, as they were seeking different contactless techniques of approving settlements. PayPal and also Venmo released QR code repayment techniques for in-store settlements, which assisted numerous SMBs to approve contactless settlements with reduced equipment combination prices.

” We refined over $20 billion of repayment quantity, with virtually 10 million customers making use of PayPal in shop,” Magats claimed. “Our services and products have actually never ever been even more appropriate and also vital for our consumers than they are today.”

PayPal has 29 million vendor accounts on its system that utilize its QR code or P2P repayment networks for approving settlements.

P2P settlements are readied to advance also better in the coming years, according to Baker.

” I believe that electronic P2P repayment techniques are coming to be a lot more usual for micro-businesses,” Baker claimed. “As well as the play [trading and crypto investing] is more than likely to be able to create income from the application and also secondarily to drive even more customer interaction.”

6. Cross-border settlements

In a globalized economic situation, a demand for quicker, less costly and also a lot more reliable cross-border purchases is gradually coming to be a requirement. Cross-border settlements were expanding progressively in the middle of climbing globalization and also less complicated cross-border purchasing before the pandemic.

According to a McKinsey & & Firm record, cross-border repayment moves completed $130 trillion in 2019, creating settlements income of almost $224 million. In 2020, profession and also traveling halted, straight influencing cross-border purchases.

Visa’s cross-border quantity decreased 29% in Q3 2020, after being up by 7% in Q3 2019, according to an Expert Knowledge record. Mastercard’s cross-border quantity sank 36%, compared to an approximate 16% boost in Q3 2019.

” We did see in 2020, a decrease in settlements task, yet in the 4th quarter of 2020 we currently saw that quantity recuperating,” Erika Baumann, an expert at Aite, claimed. “We anticipate the quantities are mosting likely to remain to boost in 2021 and also 2022.”

” Services that are making cross boundary settlements are obtaining annoyed with the rubbing and also the cross border-payments procedure, and also are seeking some choices to eliminate a few of those discomfort factors.”

Erika Baumann

Expert, Aite

Lowering cross-border settlements can be credited to an old contributor financial version that has actually remained in location for over thirty years. It has a “multistep procedure with intrinsic problems that produce rubbing at the same time,” Aite research study specified.

” Services that are making cross boundary settlements are obtaining annoyed with the rubbing and also the cross border-payments procedure, and also are seeking some choices to eliminate a few of those discomfort factors,” Baumann claimed.

In the present old-fashioned contributor financial version, a company sends out repayment directions to its financial institution. The financial institution, which likely does not have an existence in the nation of the recipient, will certainly send out that repayment to a ‘contributor financial institution.’ That financial institution will certainly send it to one more contributor financial institution that will certainly transform the repayment right into the recipient’s money.

A great deal of advancement is taking place in the cross-border repayment landscape since conventional correspondent repayment networks are cumbersome and also can take days to refine a deal with relatively high prices.

Arising markets normally obtain neglected as a result of the absence of facilities needed for contributor financial versions. Still, contributor financial institutions remain to diminish.

” If you remain in an arising area, (such financial institutions often tend) to be high threat and also reduced earnings since you simply do not have the exact same quantity of settlements,” Baumann claimed. “As well as second of all, since the innovation exists to make these settlements less complicated.”

Fintech business and also much better technical versions can aid offer a much better repayment network and also get to arising markets, Baumann claimed. This will certainly produce an area on the market that can cause a surge in payment-as-a-service (PaaS) service providers, Baumann claimed.

Visa, Mastercard, MoneyGram and also others are bring out solutions to much better help with cross-border settlements. MoneyGram lately released a solution to move cash to an electronic purse from virtually any type of location on the planet, and also currently, the business will certainly link consumers and also suppliers from all over the world too.

Visa additionally released P2P and also B2B cross-border repayment networks to much better help with faster settlements, and also lately broadened that connect with the purchase of EarthPort.

” Larger banks that have the ways are developing their very own cross-border repayment networks may attempt to do so,” Baumann claimed. “While smaller sized FIs are seeking to companion with fintech since it’s relatively low-cost.”

Comply With.

Vaidik Trivedi.

on.

Twitter.