10 retail traits to observe in 2022

Each 2020 and 2021 had been unmistakably impacted by the pandemic, albeit in several methods.

Throughout 2020, particularly because the COVID-19 disaster was simply starting, mass closures and stay-at-home orders created chaos for retailers because the world tried to grasp what precautions to take. A lot of the yr was purely survival mode, as some retailers drew down money to remain afloat and others teetering on the sting had been tipped out of business by the sudden blow to gross sales and liquidity.

After a wave of bankruptcies in 2020, however 2021 was calmer in that regard. As a substitute of bankruptcies, the yr was marked by acquisitions, IPOs and different transactions because the trade stabilized barely. The set of challenges retailers confronted because of the pandemic was totally different: As a substitute of mass momentary closures, retailers spent the yr battling provide chain bottlenecks as demand got here surging again from 2020, and introducing new perks to try to entice employees throughout a scarcity.

As we glance to the yr forward, we’ll be holding our eyes on how the pandemic continues to influence retailers, together with these 10 traits.

Retailers (in the event that they’re sensible) make investments closely of their provide chains

The world’s provide chain underwent large stress in 2021, not like something in fashionable commerce in its breadth, depth and pervasiveness. COVID-19 outbreaks, demand surges, capability shortfalls, labor shortages and different confounding components scrambled the flexibility of many to totally inventory their cabinets. Freight congestion might ease in 2022, however varied pressures and excessive prices might persist past the yr.

After a yr of emergency measures like air transport and ship chartering (for those who might afford it), 2022 could possibly be a yr for evaluating, rethinking and investing in provide chains in the long run. However will that occur?

As a latest paper by FTI’s Christa Hart, Ron Scalzo and Matt Garfield put it, “Retailers had designed their provide chains to deal with predictable and particular challenges however had not adequately invested and undergone the end-to-end structural transformation essential to change into actually agile.” Taking the biggest dangers out of their provide chains, the authors word, possible means diverting capital from different key tasks to improve the know-how and capabilities.

Till latest years, provide chain has typically been an unsexy, underfunded a part of the retail group. Nothing has illuminated the provision chain’s significance fairly just like the pandemic. With different dangers along with the pandemic, in addition to vital social and environmental imperatives, there is no such thing as a higher second than proper now to reinvent provide chains within the trade.

Retailers should rethink their relationship with employees

Uncommon was the retail earnings name that didn’t point out labor in 2021. Retailers struggled not solely to employees their shops but in addition their warehouses and logistics features, including to the trade’s provide chain woes for the yr.

Some have responded with increased wages and different perks to attract in candidates. However retailers nonetheless got here up brief. Vacation staffing was down 7.5% from 2020. Among the many unemployed, well being points had been the highest motive for these staying out of the labor drive, in addition to psychological well being considerations and household duties.

Unions and labor activist teams have pushed for stronger pandemic protections for retail employees in addition to higher compensation for the dangers to frontline and important employees. On the similar time, the Nationwide Retail Federation has labored to dam the Biden Administration’s vaccine mandate geared toward decreasing the unfold of COVID-19.

If labor stays tight within the U.S. in 2022, retailers might have greater than inventive perks to win recruits. The trade’s long-standing relationship with those who employees its shops and distribution facilities could also be up for renegotiation.

How final yr’s flood of IPOs will shake out

Final yr, a wave of IPOs swept the trade as retailers tried to get in on the recent inventory market. The vast majority of the 18 retail public listings Retail Dive tracked in 2021 got here from e-commerce firms.

As these manufacturers entered the general public markets, their financials grew to become public as properly. For some manufacturers, these filings made clear simply how onerous it’s to show a revenue whereas working largely on-line. Whereas Warby Parker helped pave the way in which for different DTC manufacturers, it’s struggled with profitability. Since fiscal 2018, the model has both reported losses or damaged even yearly. Equally, in Hire the Runway’s S-1, it mentioned it has a “historical past of losses,” reporting a internet lack of $171.1 million final yr.

There have been indicators of hassle in earlier IPOs as properly. Casper, one other e-commerce darling that made its public debut in early 2020 earlier than the pandemic was absolutely realized within the U.S., introduced in 2021 that it could be taken personal once more. The DTC mattress model in November inked a deal to be acquired by personal fairness agency Durational Capital Administration.

Casper’s 2020 IPO was broadly thought-about underwhelming and its inventory worth tanked simply months after going public. Whereas that worth has ticked up because the low of $3.18 a share in March 2020, it has but to achieve its preliminary worth of $14.50 a share.

To date, most of the DTC manufacturers that entered the general public markets in 2021 seem like mirroring the identical struggles Casper confronted with regards to profitability. However 2022 could possibly be the actual indicator of whether or not the mattress model’s public market exit is a one off or an indication of what is to return for others.

Will attire’s comeback stick?

If 2020 appeared to be the yr that lastly completed off attire gross sales, whose progress has been ebbing for many years, 2021 was the yr that breathed new life into them.

In 2020, 1.8 million grownup shoppers didn’t purchase a sew of clothes, in keeping with analysis from The NPD Group. In 2021, greater than 60% of U.S. shoppers mentioned their wardrobes wanted to be refreshed, the agency discovered. Within the first eight months of 2021, attire retailers rang up $13.3 million extra income than they did in 2019, or 10% extra, in keeping with The NPD Group Client Monitoring Service.

The momentum continued by way of the vacations, and researchers at e-commerce platform ChannelAdvisor, in an evaluation of gross merchandise worth, discovered GMV progress in attire to be up 31%. That was partly on account of increased costs. In December, Adobe discovered that on-line attire costs had been up 17.3% yr over yr and down simply 0.4% month over month, a shift from earlier years. Since 2014, on-line attire costs rose by 9% or extra throughout solely three months (August 2016, January 2020, February 2020). For the eight months previous to December, they rose by over 9% each month, per Adobe’s report.

The query now could be: what to anticipate in 2022? Moody’s expects progress to mood considerably in retail and attire subsequent yr. However the resurgence of the pandemic has reintroduced a brand new degree of uncertainty that might have an effect on how individuals gown – and spend.

And 2022 could possibly be a yr of reckoning for manufacturers like Hole and Banana Republic that had been among the many few resorting to deep reductions on the holidays.

Inflation might come for shoppers’ discretionary funds

Alongside a slew of different considerations shoppers have, inflation has joined the checklist. In November, the buyer worth index, a key measure of the price of items, rose at an annual fee of 6.8% earlier than seasonal adjustment, in keeping with knowledge from the U.S. Bureau of Labor Statistics.

Whereas different industries not lined by Retail Dive could really feel the influence of inflation extra — similar to grocery and gas — it might additionally trigger shoppers to spend much less on discretionary objects. Already, on-line costs rose 3.5% yr over yr in November — the 18th consecutive month of yr over yr inflation, in keeping with knowledge from Adobe’s Digital Value Index. Coupled with provide chain complications, some retailers have been climbing costs out of each want and alternative.

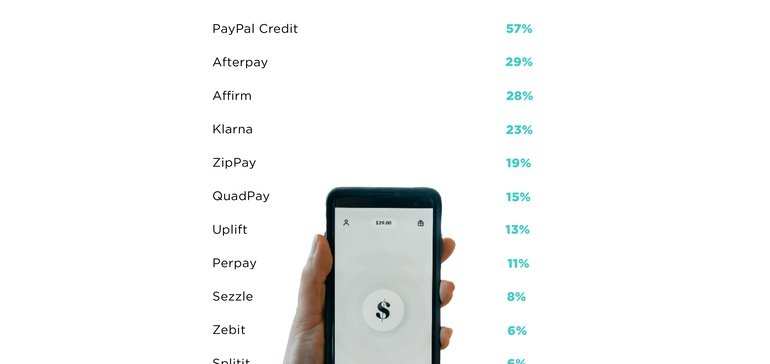

If the rising price of products persists and the Federal Reserve raises rates of interest, shoppers could lean into options to bank cards similar to purchase now, pay later to buy sure objects, which might additional influence retailers in 2022.

Retailers get cash from different companies

How do you outline a retailer? The characterization continues to evolve, as firms transfer to diversify operations and domesticate numerous income streams. It additionally means not solely providing merchandise, however companies. And, as is more and more the case, business-to-business companies.

Take Walmart, for instance. The retailer provided its supply platform to different firms through Walmart GoLocal. “In an period the place clients have come to count on velocity and reliability, it is extra necessary than ever for companies to work with a service supplier that understands a product owner’s wants,” John Furner, president and CEO of Walmart U.S. mentioned in an announcement on the time of GoLocal’s unveiling. Corporations like Chico’s and Dwelling Depot are actually purchasers.

Equally, ThredUp’s back-end, “resale as a service” platform has helped companions like Madewell, Walmart, Everlane, eBay, Farfetch and Hole navigate resale. Analysts from Wells Fargo estimate that its third-party platform, which is forecast to earn as much as $300 million by 2025, could also be extra profitable than ThredUp’s secondhand clothes gross sales.

Amazon, which is understood for its profitable AWS cloud unit, has additionally moved into different service choices. The corporate started promoting its cashierless know-how to different retailers, which permits shoppers to pay for items in bodily shops with out ready in line to take a look at.

As the price of working a retailer and e-commerce operations continues to extend, it’s possible that these examples are solely the beginning of outlets turning to different sorts of companies to herald gross sales within the coming yr.

Manufacturers attempt for the fitting stability of wholesale and DTC

What share of gross sales ought to come from direct-to-consumer channels versus wholesale continues to be a big subject of debate in retail. Conventional retailers are more and more shifting their enterprise fashions to account for the next mixture of DTC gross sales, together with well-known athletics manufacturers like Nike, Adidas and Underneath Armour. Whereas the technique can result in increased margins, it doesn’t essentially make sense for all retailers to pursue. Actually, analysts with BMO Capital Markets in September final yr questioned whether or not the channel was actually extra worthwhile than wholesale.

The result’s, in some methods, a shift towards the center. Some well-established manufacturers are slicing wholesale companions and beefing up DTC channels to reap the rewards of each fashions, whereas digitally native manufacturers are discovering worth in increasing by way of alternative wholesale companions along with their very own e-commerce and stand-alone shops. DTC activewear model Vuori, which has been worthwhile since 2017, attributed its monetary success partly to an early begin with strategic wholesale accounts, together with Nordstrom and REI.

That shift towards the center is prone to proceed, with extra manufacturers searching for the fitting stability between DTC and wholesale channels within the yr forward. Actually, Coresight Analysis predicted final summer time that manufacturers would depend on a hybrid mannequin between the 2 for the subsequent three years.

The aim of a retailer continues to evolve

Twenty years of e-commerce progress and much more years of declines of malls and the department shops that anchor them, have led retailers to drastically shrink their retailer fleets lately.

Round this time in 2019, retailers had cast plans to completely shut greater than 9,000 shops, far surpassing openings. Final yr, retailers like Nordstrom selected to not reopen a few of the areas that had been locked down for weeks because of the pandemic.

Final yr was totally different. The variety of closure plans declined yr over yr, in keeping with Coresight Analysis. However retailers, in an effort to make these shops actually matter, are additionally rethinking retailer codecs – even abandoning flagships in some instances – and switching their areas.

It’s not simply Nike, which has already made a reputation for itself with extremely experiential and neighborhood-based shops. Even greenback shops are experimenting. After a profitable debut, Greenback Common not too long ago introduced an growth of its PopShelf idea, a higher-end low cost retailer with a treasure hunt enchantment and better worth factors, to 1,000 areas over the subsequent 4 years. Macy’s and its extra upscale enterprise, Bloomingdale’s, are each making an attempt out smaller format shops in strip facilities which might be extra prone to have a Kohl’s or Goal. And Shoe Carnival, after a concerted effort to shut down underperforming shops, is now opening and transforming shops, in an effort to upend the low cost footwear market.

In a quest for larger market share, personal labels proceed to proliferate

Gone are the times when retailers connected their names to low cost, plain and low-quality personal label manufacturers. Now retailers deal with personal labels as worthwhile progress engines that permit them to nab extra market share. Retail generalists, house retailers, athletics retailers and others have all launched their very own personal manufacturers they usually don’t seem like slowing down anytime quickly.

Goal grew its roster of personal manufacturers to 48 final yr — 10 of that are price at the least a billion {dollars}. With eight manufacturers already launched final yr, Mattress Bathtub & Past beforehand mentioned it plans to launch at the least 10 personal labels as a part of its broader three-year turnaround plan. Gamers like Foot Locker, Dick’s Sporting Items and Peloton have additionally carried out their very own personal label methods.

With inflation taking maintain, personal labels could also be positioned for progress as consumers care extra about getting essentially the most for his or her buck. When the price of items outpaces the expansion of wages, personal labels could change into extra interesting to price-conscious shoppers.

Apple’s iOS updates rattle retailers’ advertising methods, particularly for DTC manufacturers

With Apple’s public launch of the iOS 14.5 replace earlier this yr, the corporate required all apps to undertake the AppTrackingTransparency framework. By way of the replace, apps wanted to ask for consumer’s permission to trace them or entry the gadget’s promoting identifier.

This created issues for entrepreneurs and retailers, particularly for direct-to-consumer manufacturers, which traditionally depend on third-party knowledge for buyer acquisition and retention.

“One thing we’re seeing that is very troublesome on the DTC facet is that the iOS 14 updates are making it very troublesome to search out profitable return on funding like we as soon as noticed,” Alex Tune, CEO of progress acceleration platform DojoMojo, advised Retail Dive in 2021. “What which means now could be everybody really has to scramble and get hold of new advertising channels which might be going to yield extra worthwhile return as a result of sadly, on this second in time … the nice outdated Fb, Instagram channel as a advertising enviornment will not be as accessible or reliable because it as soon as was.”

Corporations are having to show to different advertising channels like e-mail, SMS and even print promoting to attempt to get shoppers to buy with their manufacturers

Comply with

Daphne Howland

on

Comply with

Ben Unglesbee

on

Comply with

Cara Salpini

on

Comply with

Kaarin Vembar

on

Comply with

Caroline Jansen

on

Comply with

Maria Monteros

on